Blog/Polling

Trump inflation approval crashes to record low

The economy and cost of living are going to be major issues going into the US elections in November. That much is obvious. Given the sheer size of these two issues, it’s worth breaking them down further to understand how voters actually conceptualize the broad and nebulous concept of ‘the economy’ in practice, and what this tells us about how the country is going to vote in five months’ time, beyond the headline numbers.

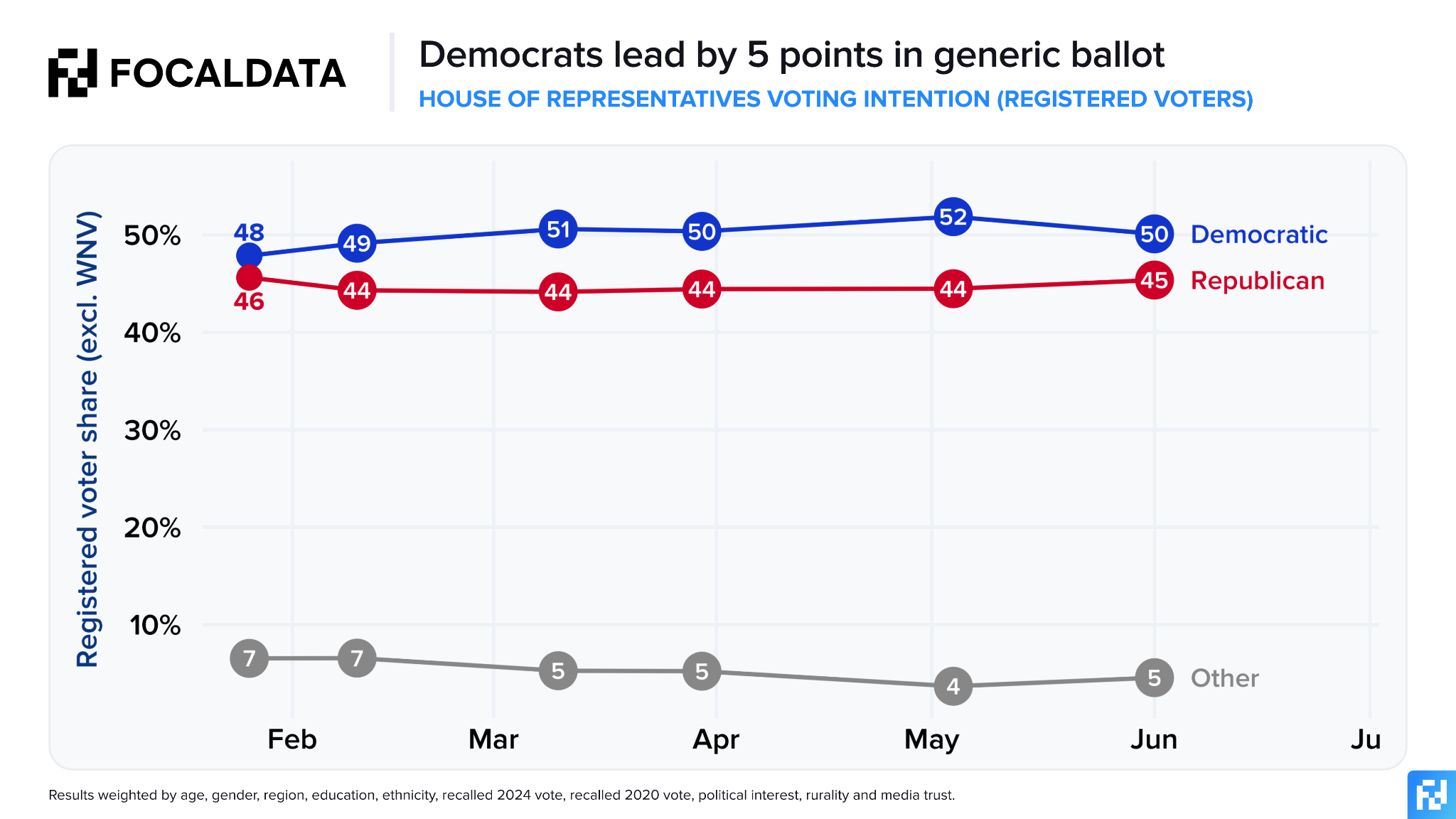

Our latest poll, conducted between 29 May and 1 June, and the latest in our polling partnership with the Financial Times, shows the Democrats ahead by 5 points in the congressional generic ballot, at 50% to the Republicans’ 45%, a small reduction in their lead since last month.

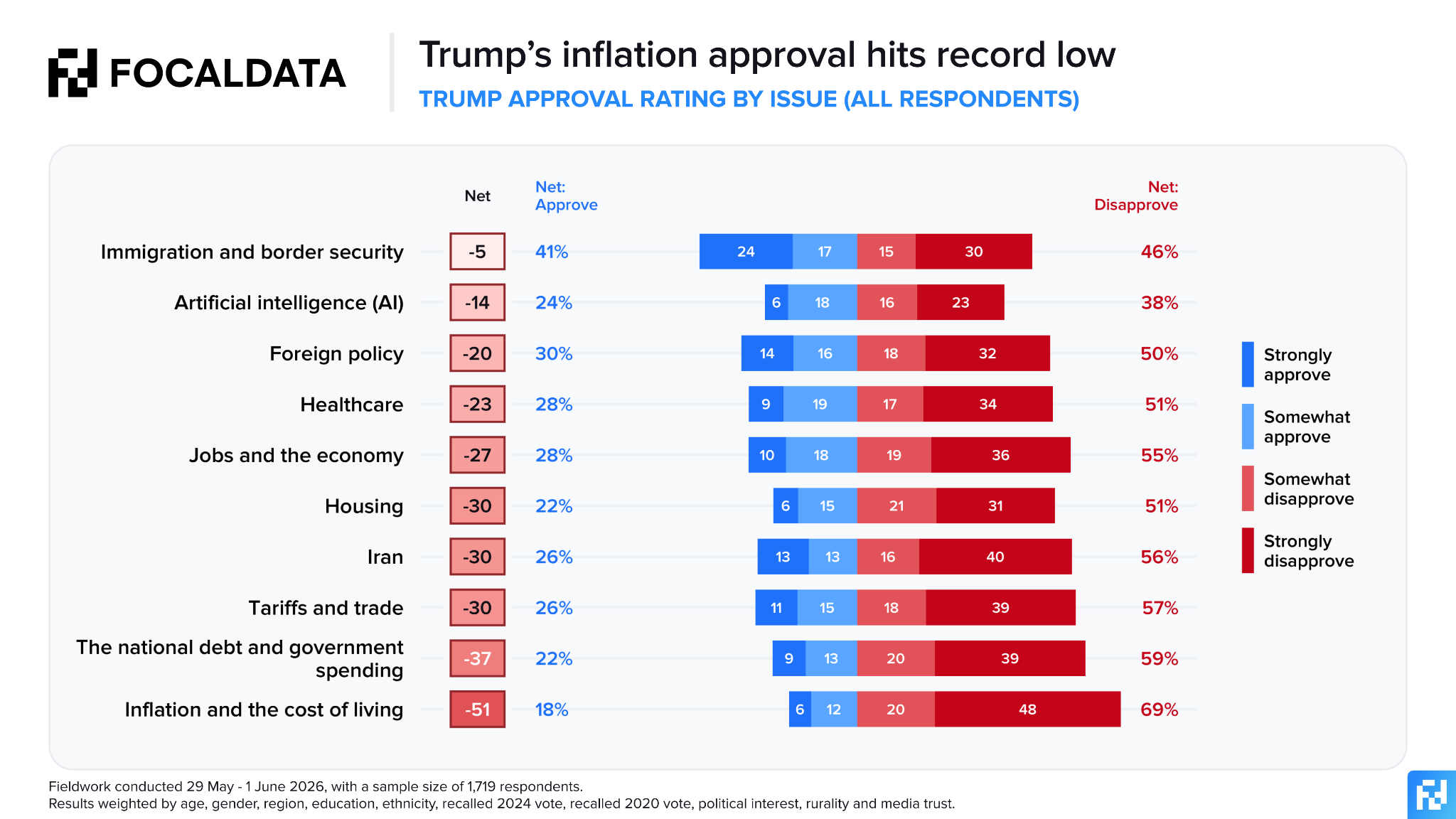

Donald Trump’s approval rating remains fairly static, at -19 overall. 37% of Americans approve of the job the president is doing, with 56% disapproving. On the individual issues, though, we see some big shifts, with the president’s net approval rating on inflation and the cost of living falling off a cliff and collapsing to a new low of -51, down 20 points in the space of a month. Just 18% of Americans now grade his performance favorably.

Even with his own voters, the president is underwater on inflation. Only 36% of those who voted for Trump in 2024 back his performance on the issue, with almost half (46%) disapproving.

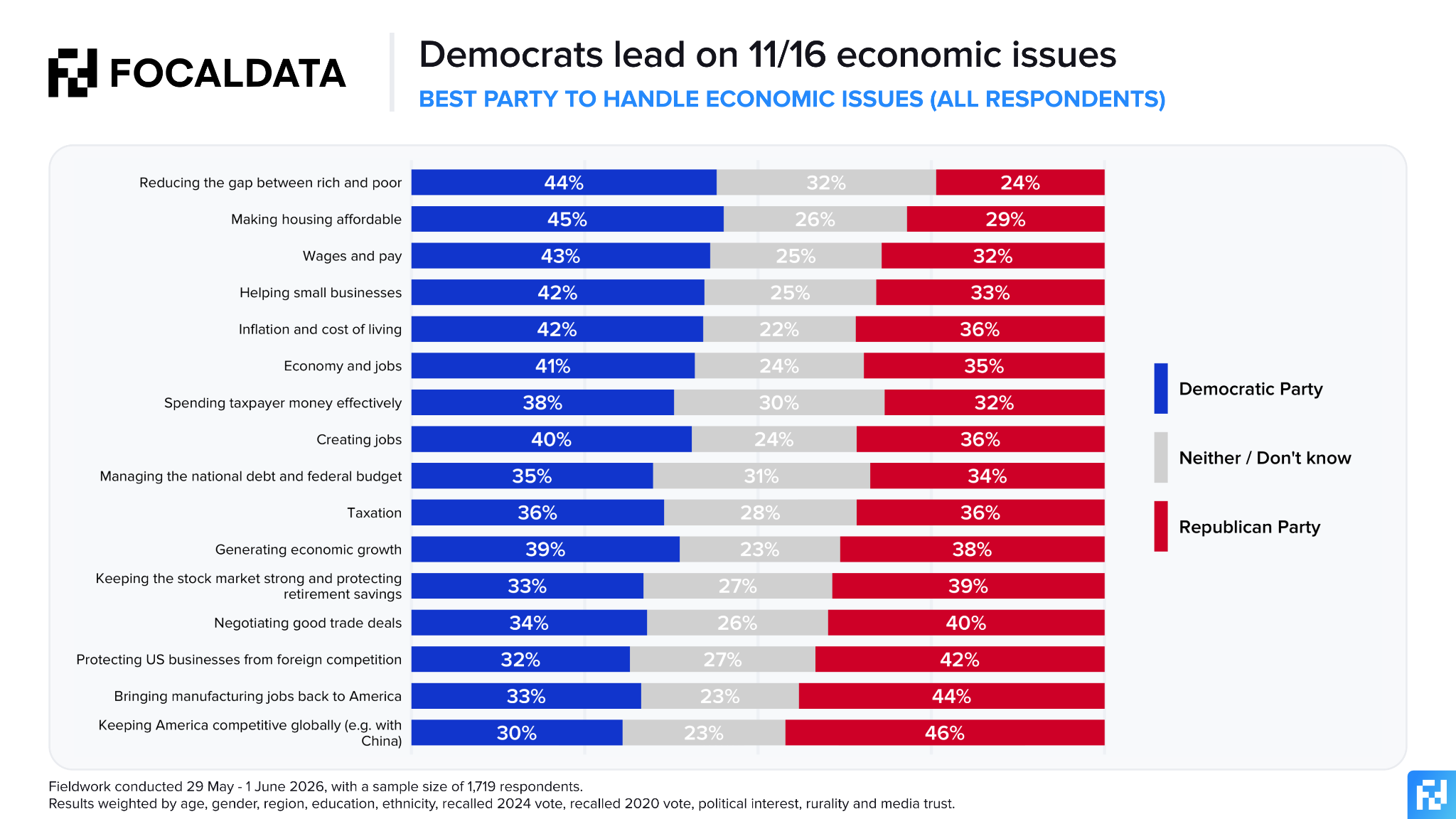

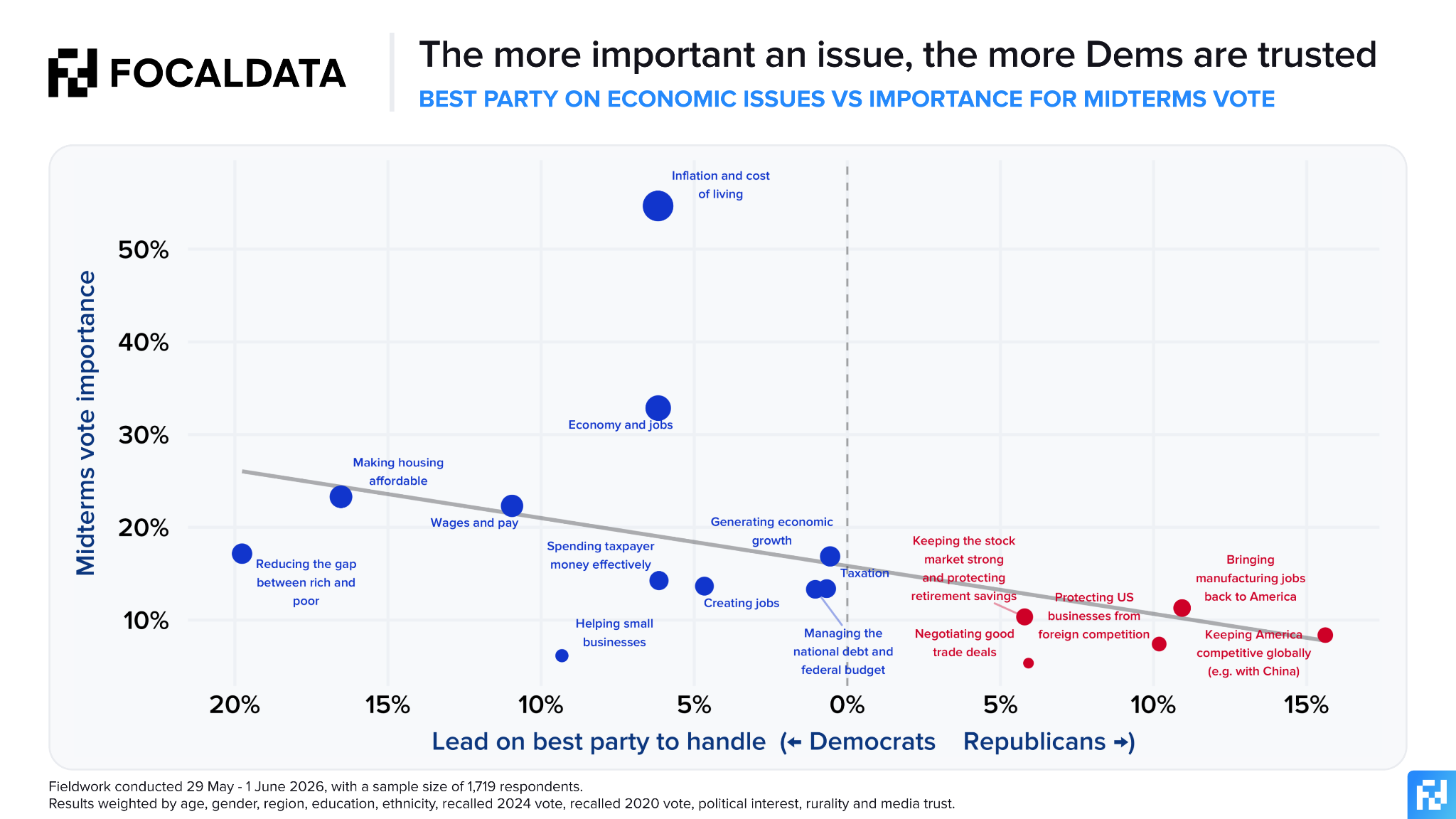

A typical pattern we see in political polling is that parties of the left are more trusted when it comes to a ‘cost of living’ framing of the economy, in which an emphasis is placed on areas which most acutely affect the household finances of those on lower incomes, but parties of the right are more trusted when the question is framed under the management of ‘the economy’ more generally. We wanted to see whether this is still the case in the current circumstances and – given the importance of the economy to this year’s elections – begin to unpick the whole spectrum of economic issues and understand the array of topics which lie between or around the two poles of personal-versus-national economics.

While we do see some divergence on those two main frames looking at Trump’s approval ratings (his -27 net score on ‘jobs and the economy’ is slightly more muted than his catastrophic -51 on inflation), that gap is entirely absent when it comes to party-level issue handling. The Democrats rack up similar leads on both the cost of living and the economy more generally.

Over the last 18 months, the Democrats have successfully burnished their reputation on the economy, and are now seen as the best party to handle ‘the economy and jobs’ by 41% of the public, compared to 35% who say the Republicans are better placed, a 6-point lead identical to that on inflation and the cost of living. Republicans are more competitive when it comes to generating growth (D +1), taxation (D +1) and negotiating trade deals (R +6), where we still see the typical bifurcation going strong.

Inflation, jobs, and affordable housing are the top three motivating factors for peoples’ votes ahead of November. Trade, protectionism, and international competition – all more abstract, global issues where Republicans score relatively well – rank at the bottom of the importance scale. Across the board, we see a clear pattern which is killing the Republicans in the polls: the more important an economic issue is to voters, the more they trust the Democrats to handle it. That is a huge red flag for Republicans in Congress, and points to a much more structural rather than transient lead for the Democrats on the economy in this election cycle.

Gas prices in particular are driving a wedge through Trump’s winning 2024 coalition. Those who chose the Republican ticket in November 2024 are more likely than average to say the cost of gas is one of the parts of the economy which affects them and their family most, with a majority (51%) selecting it in their top three factors when asked (compared to 41% of Kamala Harris voters).

The issue is of particular relevance for the Republican coalition, and the numbers will make for difficult reading for House Republicans. The just-under-half of Trump voters who say they need to buy gas for work (either to commute or as part of their job role) are much more likely to say they will vote Democrat in November. Among those who do not need to buy gas for work (either because they take public transportation or are not currently in employment), 6% intend to vote for the Democratic candidate in their district. For those whose paychecks are being diluted by surging gas prices, that figure doubles to 12%. Do not be surprised, therefore, if swings in November are amplified in suburban areas with high commuter numbers compared to inner cities or rural areas.

Our polling methodology is designed to account for non-response bias by weighting to a number of population targets where polls have often missed some respondents, specifically those with low levels of political interest, lower levels of institutional trust, and those who live in rural areas (all areas which have favored Republicans in recent cycles). While the Democratic lead in our Congressional generic ballot polling is lower than some recent polls which put the party’s headline advantage in double digits (one showed a lead as high as 14 points), I think the lead is fairly structural. If I were a Democratic strategist, I would feel more comfortable with a 5- or 6-point national lead given the economic fundamentals covered above, compared to a 7- or 8-point lead in a ‘normal’ cycle where fortunes could be transformed by rapid changes in issue salience. If anything, Democrats should be asking themselves why they aren’t further ahead.

Data tables for this survey can be downloaded here.